Welcome all to the May 26Edition of the Carnival of credit report stories!

Editor's Pick

Debbie Dragon over at Destroy Debt talks about how to stop debt collector harassment.

This is a great list to keep in mind and to have a little victory with the debt collectors if this happens to you.

Thoughts From a Former Bill Collector gives 4 great tips when dealing with debt collectors.

The overall point is to be honest and straightforward. No one's gonna help out someone trying to make their job harder.

Until Debt Do Us Part gives us 10 pieces of advice when dealing with financial institutions. Mike also talks about working at a credit card insurance phone bank.

I did this too for about 3 weeks one summer and it was hell. I have a great radio/phone voice but I couldn't sell water to someone on fire.

Life, Money, & Development talks about his love of credit cards and how he thinks they aren't as evil as people think they are.

While I think Herrera makes the point that sensible credit card use is a good thing (especially for the credit score), he also says he uses them to amortize gadget and gift cost. This mentality is how I got into trouble with credit card debt. It is a very fine line that represents the difference between good and bad credit use.

FinancialZip talks about snowballing his snowflaking.

Sounds cold, but a good way to combine 2 heavily promoted concepts.

leaving the folks talks about how all your bills can effect your credit score.

The only advice I didn't fully agree with was cancelling credit cards you're not going to use. I say throw them out or cut them up, but don't cancel them. Unused credit limit can only help your score from what I understand.

Money Blue Book talks about how to and where to apply for instant credit credit.

Just be careful to walk that thin line from above if you get the credit.

Her Home Blog talks about 3 things that show up on your credit report, and stresses honesty.

As before, be straightforward and honest and they can't get you for anything.

No Debt Anymore.org starts off a 5 part series regarding Credit Repair and how to get your free credit report from the big 3 agencies.

Knowing is half the battle. Go Joe!

Thanks for reading, everyone. And if you feel so inclined, head on over to How I Save Money.net to sign up to host either the Carnival of Credit Report Stories or the Carnival of Twenty Something Finances.

Carnival of Credit Report Stories - May 26th Edition

Monday, May 26, 2008

Frugal health?

The wife was told she had high cholesterol, and I am sure I do too, but haven't gotten a check up in awhile, so we need to go healthier. Buying more fish, veggies, and fruits. I bought a food dehydrator today to make the fruits store better for $60. But after looking at the mechanics of it, I think I can make a larger industrial sized one out in the yard on the cheap based on the solar oven. I think I am going to put it out in the greenhouse, which also got a fund boost this week.

Seeing as I will no longer be in my twenties by the end of the week, I have started getting some birthday funds. Got $50 from the in laws, ad we are heading out to Lowe's later today to see what we can get for the price. I am looking at getting some plastic siding and some zip ties to surround the dog pen we have. I was also looking at 8' folding tables to place the garden boxes for square foot gardening on, and they're $40-60 a pop. That's ridiculous, so I am looking at alternatives.

But the seeds are growing, the peppers need to be transplanted, and we finally got a sprout out of the tomatoes. w00t!

Wow. What a week.

Sunday, May 25, 2008

It has been one of the busiest weeks ever. Long story short, I worked a bunch of hours, the wife's car got totalled, we have to switch to a healthier diet, and we bought a car. Now for the long story long.

We heard last Saturday from the insurance agency. Here car was totalled out, but because she didn't drive it a lot, we got $4050, then minus the deductible, so we cleared $3050. Then we were faced with a new dilemma, do we exactly replace her car, which we could have done with the money we got, or do we step up a little step and get a four door and finance?

She did have a 1999 2 door Sunfire. We got it in 2001, and it served us very well. It never needed any real work, and got us where we needed to go. But, it was going to need to go in about 1 to 2 years to accommodate a family in about 3-4 years and still have some trade in value. At that point we will need to be looking for a 4 door. Well, we decided to step up a notch and finance (some of) a car now that will fit our needs for the next 5-7 years, instead of buying a car without financing now and not have it really fit our needs now or later, but not finance.

So the wife went online and started looking last weekend, thinking that we would be able to go car shopping during the week. I thought so too. Then we found out that lots are not open past 6. What?!? How do you sell cars then, good sir? We did find out that lots were open late on some days of the week, so I figured we go on that day. Well, work intervened, and I worked late every day this week, so we were not able to really go looking until Friday.

Friday rolls around, I have the day off, and we get a list together. 1 car is in the opposite direction by about 30 minutes, so we do that one first. Well it is a small lot, and we get there only to find out the car we went to look at had been sold. We go to another lot, and the car's not there either. You gotta be kidding me! Update your damn websites. So at this point the lots were closing because we got a late start, and we only made it over to the neighboring lot to see if she liked the styling of one of the cars, even though the car was $12000. We knew we weren't going to get it, and so did the dealer, so we sat in it, and the wife liked it, and we home with the equivalent of blue mufflers.

So we got a plan together for the next day, went to see the style she liked and got it. Almost. Since we are still trying to fix the financials, the bank needs to talk to my HR company to verify employment before we can finalize anything. But we are able to stop looking. We ended up getting a 2002 Ford Focus ZX5 for $7200, at $200 a month for 4 years. Way to go bad credit! We'll be paying $200 a month for a year, and then use next years bonus money to pay off the car in full. At least this time we have a plan.

More on the health stuff in a later post.

Don't forget the Carnival of credit stories will be hosted here tomorrow!

Drained

Tuesday, May 20, 2008

I am mentally and physically drained. I do not know how people work 12 hours a day on a regular basis for their job. I know there are those people out there, and I applaud them. I am working on another "important project" this week. Tomorrow is the last day for data acquisition, so that's a plus. The results are turning out well, also, but man is it draining. I've gotten home at 8 the last two nights, and I've gotten into work around 7 - 7:30 the last two days. Then on top of that, I start another "important project" on Friday. Ugh! At least I am in high demand. The only real problem is that this project and the next one are for my boss' boss, and my boss is still concentrating on the project I finished last week, and I don't have the time to concentrate for him. Not the worst dilemma to have, but it is draining.

On a better note, I was featured in the two carnivals I submitted to this week. Check out the Festival of Frugality over at the The Financial Blogger, and my post aboutyour retirement picture. Also head on over to the Carnival of Debt Reduction at ptmoney, and my post about an interesting morality issue with one of my debts.

Thanks to alpha consumer. I got my copy of "How You Can Profit From Credit Cards". I will be reviewing it once work calms down a little bit.

I will also have a guest post tomorrow over at money and such about the return on investment on fuel saving devices. Make sure to check it out.

On May 26th, I'll be hosting the Carnival of Credit Report Stories. Make sure to submit your stories by Sunday May 25th to be included!

image by KM&G-Morris

The social pressure we put on ourselves

Sunday, May 18, 2008

image by CaptPiper

Recently, Trent over at the simple dollar posted about how he and his wife won't put up a clothesline in their backyard because of the negatives due to societal pressures they perceive, such as lower property values, and the scorn of their neighbors, even though it is the more frugal choice. They figured it would take 89 loads to break even with the cost of installation. I am sure they would hit this number some time this year also.

This post popped into my head during church today. I usually prefer to wear jeans to church since if I were to dress up I would wear the same clothes I wear 5 days a week. It is the weekend, I do not want to wear those clothes. However, I feel guilty every time I get to the parking lot because I see that a large number of people are dressed up and I perceive that they are looking down on me because I am not dressed up like them. I have no clue what they are thinking. They may be looking down on me, But I am willing to wager that far fewer of them care than the number I imagine. After all, I am there to worship, not put on a fashion show. This is also one of the reasons that I don't go to the same Church as my boss, and the vice president of my division. These people dress very nicely every day in the office, and I believe that they are also the type to dress very nicely at Church. If I went to their Church, then I would feel even more pressure to spend more money on even better clothes. I would probably be promoted faster if I went to their Church, but should Church be associated with networking? I don't think so, so I don't go there.

But would Trent's neighbors be mad at him if he put up a clothesline? Possibly, but they might like the idea also and decide to put one up. If all the houses have respectable looking clotheslines, would the property values go down? What if they used 4x4 painted posts with lights on top, and a retractable line in between, and maybe even a small garden around each post? Would that increase property values due to better landscaping?

The point is that are there as many societal pressures as we perceive, or are there other people around us, who think like us, but are also afraid of their neighbors and what they may think?

On a side note, Trent brought up the point about how many frugal ideas have been associated with being poor, and how the frugality of the WWII generation has been lost since then. I waned to point out that my grandmother's old house was so frugal that it had an exterior door that opened almost directly to the clothesline. This door was only 4 feet away from sliding glass doors, so its only purpose was to make taking clothes out to the clothesline easier.

daily goings on

Friday, May 16, 2008

I WON!!!!! My submission for how to best spend $1000 won over at Alpha Consumer It seems like my new ways of thinking about money are on the right track, at least according to her readers. Too bad I didn't win $1000, but I did win How You Can Profit from Credit Cards by Curtis Arnold. I'll be reviewing for the site one it arrives.

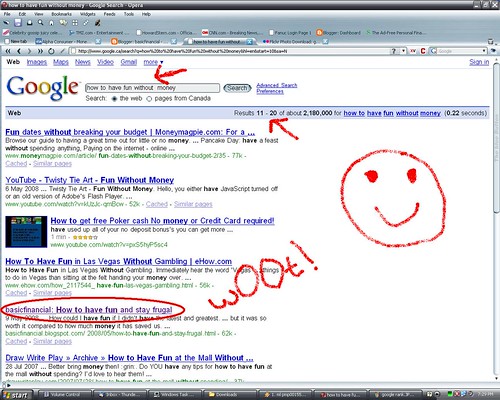

I also seem to be on point with my money ideas according to google. My post on How to have fun and stay frugal landed at number 15 on "how to have fun without money.

It also seems that my post on the hydro 4000 is getting a bunch of hits from google, too. If you found that article interesting, check out money and such in the coming week or so for the follow up article concerning the return on investment for fuel saving devices.

And alas, the emergency fund had to be tapped into today. It now stands at a measly $50. My wife got into a car accident yesterday, ad the car will most likely get totalled, since it is not worth a whole bunch. We have a $1000 deductible, and the e-fund will go towards paying that. It mi gt get a replenishment depending on the vehicle we buy, so here's hoping for a large settlement from the insurance company. And please keep us in your prayers, she is not very seriously injured, but is shaken up a bit and has some whiplash and pretty decent bruising.

Not being frugal with my wife

Thursday, May 15, 2008

My Open Wallet talked about how her relationship does not always strengthen her frugal mindset. I can totally agree with this.

My wife is probably my biggest budget buster. She does not mean to be, want to be, or try to be, but I love buying her little things. I will usually rationalize buying her some flowers, a stuffed dog, or some other little item way more often then I should. I just love seeing her smile. I have tapered off quite a bit since starting this blog, but it could get expensive with in between $5-$10 a pop. We both have the same mindset about budgeting, but it is so hard for me to tell her no, or to not buy her some little item that she can put around her desk.

I wish I had a better handle on the money so that I could do this more often.

Go go gadget emergency fund!

Wednesday, May 14, 2008

Paidtwice wrote about starting an emergency fund even when you have debts to pay off. This is a topic that is near and dear to my heart right now, being new to the whole financially responsible lifestyle.

It fills me with pride that I currently have $250.20 ( $0.20 free cents I might add due to interest) in my ING direct account. It will soon swell to over $350 as soon as my bi-monthly $100 clears. I still owe on debt, though. I have been keeping my head in the sand about most of it for quite some time now. The reason is because I was one of the "I can't save any money or pay down my debt because I am always playing catch up." As of April 3rd, 2008 I made a vow to stop using this as an excuse to not have an emergency fund, to not fund my retirement, to not get my company match on my 401K, to not live financially responsible.

I know that as of this minute I am not living completely and 100% responsible because I owe people money that I am not paying. But at least right now I am making steps to correct the problem, where as before I did not even care. The benefit of my emergency fund is that when something bad comes up I will to need to miss bills, or go deeper into debt to pay it off. I will be willing and able to pay cash. This is such a foreign concept to me, but I love it. Even when I do start paying down my debt, if I have an emergency, I won't need to stop paying my debt. I can use my emergency fund.

So I am very much in favor of the e-fund as a starting point for financially responsible living. Paidtwice makes a good point that it also makes a saver out of a spender. I was an uber spender. When I couldn't pay my mortgage, and we got our deposit back from the utility company, we bought a Wii. Yes, I said that right, and it makes me both sad and mad that we did that. You want to know the economy is in the crapper? It's because of people like me. Or at least people like I used to be. Who in their right mind would buy a Wii instead of pay towards their first mortgage not 6 months after buying a house? I remember the rationalisation I made at the time. It's only $200. That wouldn't make a dent in my mortgage payment, and we'll save money in the long run because we will stay at home more. Yeah, right. That didn't work out. But that's the mindset of the subprime mortgage meltdown.

It took my friend who makes less money telling me he paid off his $4000 credit card debt with ING.com account to wake me up. He just paid off more than my past due debt making less than I do. Why I am living this way? My emergency fund helped to get me out of the spending mindset. I could not be more proud of my $250.20. It makes me more proud than owning the hot video game system, or the ipod or anything else. My e-fund made me proud at $50 the first day, at $150 when the first automatic payment, and it will make me proud when it is up to $2000 and we start paying off debts we haven't touched in years.

If you are just starting to get your finances together, the e-fund is definitely the way to start.

What's your retirement picture?

Plonkee over at plonkee money posted that she is not really able to picture what the retirement life will entail. Plonkee works a conventional job that she likes and wouldn't mind working until she can fully retire and at least not have to worry about what job she works, or if she works at all.

I am pretty much in the same camp. I work for a great company, I like my field, and while I loved what I did at one time, I still think it is the right company for me. I totally dig the people and can see myself working there until I retire from my industry.

I have a 2 stage retirement plan, though. I get paid pretty well for my age, around $70,000. The problem is is that my wife and I live in a fairly high cost of living area. My first stage is to save up enough for us to live on from the age of 55 on. Now we may have enough to do that within the next 10-15 years, well before the age of 55. I would like to teach high school at this point. Move back to my hometown, teach at my old high school, make enough to pay our bills, start building our compound and esae into retirement.

After I either a) decide not to work anymore, or b) reach that oh so sweet age were we can live off of interest, fully retire, pull the drawbridge up, and relax with the wife, the animals, and do whatever the hell I want, and not care.

daily goings on

Tuesday, May 13, 2008

Work is going nuts right now. This is my busy time of year, and i keep getting lined up for more and more projects. The really annoying part is there are a couple people line me up for projects, let me know the projects are going on, and then tell me I am doing the project the day before it starts. Arggh. Well on to more fiscal matters...

It looks like Financial Learn did not read my post on the hydro4000. They're pormotong running your car on water. It's a short article and it does have one incorrect fact. They say you can run your car on tap water. While technically true, it is not suggested for more than a one time use due to the impurities in the tap water.

Also, I'll be guest posting over at Money and Such next week. It'll be a followup to my fuel efficiency devices post.

Please vote for me!!!!!!

Monday, May 12, 2008

Kimberly Palmer at Alpha Consumer asked the question "What would you do with $1000?" I posted the following response

Use it to save more money: The first thing I would do is buy a decent bicycle so that I could bike to work (on non-rainy days), since I live only six miles from work. This would cut down on my gas costs, especially if I start now. I would also convert a dog pen we have into a greenhouse to grow my own veggies and sell the rest at the local Farmers Market down the street. I would also probably put in between $400 to $500 into our emergency fund.

I was chosen as one of the top three. If I win it would be pretty cool. Please go to Alpha Consumer to vote for me! Please!?!

First Carnival!

I was mentioned on someone else's website! w00t w00t! Check out the Carnival of Personal Finance over at Money under 30.

Morality and debt

So here's a tricky one for you. My largest single debt is $1400 I was on a payment plan with them, but when I checked my credit history, the account was not updated to show that I was paying on it, thus bringing it out of the realm of really bad debt to only bad debt. I contacted the company, and they said that they do not report to the credit reporting companies until the debt is paid off. I found this to be rather shady, so I contacted the credit reporting agencies to tell them that the debt history was inaccurate. I waited 30 days and the final response and the credit bureau reported back that they got no response, which meant that the debt was wiped off my credit history.

So the dilemma is that even though this is money I owe, and will eventually pay off, it is a debt that does not affect my credit history negatively, or in any way. What would you do in this situation?

New Logo!

Sunday, May 11, 2008

Well, I finally got off my butt, and onto GIMP this morning. I've been meaning to make one for awhile now, and finally did. w00t! I think it fits the minimal style that I try to keep with the design, and I dig the color styles. I thought about going orange and white but that wouldn't match the banner that I also really dig, so greens it is. ![]()

Let me know what you think!

I can save how much on gas?

Saturday, May 10, 2008

As I groggily lay in bed yesterday morning, punishing my snooze button, the local news ran a story about how to dramatically increase your gas mileage. They had me roped in, but I was skeptical that it would turn out to be the same old "don't mash your gas and brake pedals" line. I was wrong.

Instead it was a story about the hydro4000. An affiliate news station did a study on this fuel saver with one of their news vehicles, I think a Ram 1500. They attached this device to their engine for 30 days. Their gas mileage went from 9mpg to 23mpg. Hooey or not, I was interested. Being a fluids guy myself, I figured I'd be able to see what was really up, and expose this whole scam.

How it works

The hydro's website says that it turns your engine into a hybrid hydrogen fuel cell. While I think this is a vast stretch of the terminology being used to cash in on buzz words, there is a little bit of merit to it. After visiting the website, it is not exactly clear on how the technology works with your current fuel system, but the new cast said that it injects Hydrogen into your pistons' cylinders at the same time that gas enters, which will enable your gas to ignite more efficiently. So far, their basic concepts are holding up. Your engine does not ignite all of your gas, and a more hydrogen rich environment will both a) allow more gas to ignite and b) give a little boost when the hydrogen ignites as well.

The sensationalist part

The sensationalist part comes in partly from their website, and partly from the newscast. Their website states that you will see, on average, an increase of 30% fuel efficiency, not the 150% increase that the news team found. This makes me wonder what other maintenance was done around the same time to the news vehicle. The website does it part, too though, when they throw out one liners like, "Imagine a world free of Carbon Monoxide gas, the major pollutant created by industry and vehicles." This device will not produce those results. It is still used on internal combustion engines. These still produce greenhouse gases.

Impression

With a $1200 price tag, it doesn't come cheap. I'd like to see it in use for sometime also before I put on my car. One drawback to this system, too, is that it requires distilled water in the tank. Now, I don't know about most people, but I don't have a table top water distiller sitting next to my toaster. But for an extra $110-$150, it would only increase the overall costs by around 10%. But hey, if it works, it works. And with gas costing around $4.00 just about everywhere pretty soon, you would only need to fill up 1125 gallons before the unit and the distilled water unit payed for itself. For me that would be 56.25 fill ups, or 1.5 years.

How to have fun and stay frugal

Friday, May 9, 2008

One of my biggest fears in switching from an uber consumerist lifestyle to one of frugality was that I would be bored. How could I have fun if I didn't have the latest and greatest. As it turns out, I am having a blast learning about new (cheaper) things and enjoying the items I already have. I've also come up with a few creative ways to get some very enjoyable new (not so cheap) items.

One of the things that I have found to be very enjoyable is an old xbox, not the 360. The main reason I find this to be fun is because of XBMC. While this bit of hacking does void the warranty, it is extremely simple to load and expanded our entertainment choices in our house by a very significant amount. We were able to connect it to a wireless bridge and now have a wireless connection to our computers on our TV, which is great for watching movies or listening to music when we're not in the office. I ended up buying the xbox for $60 at our local gamestop, and I had to search and go to best buy 7 times and spend $100 to get the networking just right, but it was so worth it compared to how much money it has saved us. Also, with prices now it would cost about $100 to get the whole system set up, given that you have a wireless router already, which we did.

I've also gotten into <gardening. I am anxiously waiting for my beefsteak tomato sprouts to come up. They are very tasty.

Another way I was able to receive my favorite toy is through gifts. It seems to be somewhat overlooked way in the personal finance blogosphere, but it worked great for me. A little before Christmas I decided that I wanted to get an electric guitar. I have played my acoustic for about 7 years and never really done anything fantastic withit since I have short pickle fingers. I have a 20 year old trumpet that I played in band in high school. I haven't played it since, but my mom bought it for me and I didn't want to sell it without her ok, which I did not get. This is when I found craigslist. They had some starter packs for $100 to $150. This was so out of our budget it was ridiculous. We were still trying to dig ourselves out of paying for our wedding, and barely could cover our mortgage. So my wife brokered my parents (who are divorced and this is no small feat) and my sister, and they all chipped in to get me the starter pack I wanted. It cost us nothing, and I got a sweet new toy that I enjoy at least an hour a day, and sometimes 5 hours.

The third way I was able to finagle some new gadget was the ever hated extended warranty. A couple of years ago I worked some significant overtime, and was able to buy an 8gig creative zen mp3 player. It cost $200 at the time, and I payed an extra $0 for the warranty since I am hard on my items. About a year later, it died. So I went in to Best Buy and told them I needed a new one. The service clerk told took my old one and told me I had $200 on anything at the store. Well, Ipod nanos had come down in price and up in volume, so I got one of those. I was still in the extended warranty time frame, so I was still covered with my original $20. Dig it. Well, about a year after that Apple came out with the video nanos. I thought about pouring water into the headphone jack, but had obvious moral issues with that one. But, when the ipod started resetting itself when I would play a particular playlist, I took it back again. They refunded it and I got an 8G video nano. All for spending $200 almost 2 years before.

What are your creative way of having fun while remaining frugal?

Rock Bottom / Frugal Wedding Followup

Thursday, May 8, 2008

I posted about our frugal wedding recently, and I thought I would follow up with the massive financial mistakes that we made while paying for our wedding.

The first mistake we made was not properly saving, even though we were engaged for over 2 years. Since we are the fiscally irresponsible types that nickel and dime ourselves to debt, I can only remember a few of the items that we actually bought. We bought an entertainment center for $300. We still have that, and it does look nice, but I don't think it was necessary. Another thing we bought was my $200 mp3 player. While this turned out to be a good investment (I've gotten 3 mp3 players with that same $200, which isn't that bad, but my $40 mp3 player would have lasted and done a good enough job until after the wedding. We also moved and since we were renting a house, this meant a security deposit worth about ~$1800. This amount alone was worth ~1/3 of our overall wedding expense. Now we were paying $400 less per month, which turned out to save us money in the long run, but if we hadn't had the extra $400 a month, we would have not spent it either, especially if we had socked away the security deposit.

By far though the stupidest mistake we made was charging some of our wedding to my company credit card. I work for a fairly large company that did not check the card purchases until you didn't make the payments. This happened shortly after our wedding.

We also bought a house a month before we got married. While this also turned out to be a good investment, it would have reduced a lot of stress. It turned out to be a good investment in the short term because without any out of pocket expenses, and having a craptacular credit score, we walked away with $1200, which was just under 1/6 of our total wedding expenses. We got an FHA loan, and my now wife filed the paperwork to get another company to pay the 3% downpayment, and the seller agreed to pay the closing.

Since we didn't save for our wedding and were living check to check, the final expenses of our wedding took us by surprise. Way too many little tic-i-tac stuff that added up quickly. We went overdraft on the day of our wedding. Luckily, our bank allows overdraft to a certain amount, so we had enough juice to get gas and get back home from the wedding. We were not able to go on a honeymoon because we were broke. Throughout the course of the following week, all the checks we wrote on our wedding day continued to clear, sending us deeper and deeper into overdraft. I'm talking finance charges out the ying yang. So during that week I got a check advance so that we could buy groceries. Checks continued to clear, sending us back into overdraft.

By the end of this week we were out of money. I could not get another check advance, and we had reached our overdraft limit at our bank. I felt like a failure because here I was not married for a week, and I could not provide for my family, even making $65K a year.

So payday comes around a week later, and we can once again afford groceries, and luckily we had just bought a house so we didn't have to make a mortgage payment, but with the overdraft charges and the payday advance due, we could not pay all of our bills, including the final charges of over $2000 that was put on the company card. So, I got another payday advance. I paid a portion of the credit card bill, but I couldn't pay it all. Another month went by, and we had pared down our nickel and diming expenses. But we still couldn't make all of our bills, including the corporate card. So, I missed making the very first mortgage payment. Another month went by, and I got a notice from the human resource department. So did my manager. I had to come clean, and I had to pay the balance, which was $1400 by this time. So, I missed another mortgage payment. Talk about feeling like a loser. Out of 3 mortgage payments I could have made in my life, I made 1. It was not that I overbought the house. The payments, everything included, was only $1414 a month, less than $200 a month more than what we had been paying for rent for the least year and a half.

We are just now coming out of paying for our wedding. This should be the first month that we don't go overdraft, or don't get a payday advance. I am very proud of this, but I wish that we hadn't had to go through all that other crap to get to where we are.

Grocery Roundup

Tuesday, May 6, 2008

Checked out the Kroger's on the route home today. Here's the roundup:

Basics: $32.17

Home items: $10.18

Indulgence: $6.00

Side Dishes: $7.51

Quick Meals: $0.00

Cleaning Products: $0.00

Coupons: $0.00

One of the reasons why I stopped by the store is because I read The Simple Dollar talked about how he bulk makes rice and bean burritos. That got the taste in my mouth. I spent $7.53 on ingredients for beef and bean burritos, and was able to make 9 of them for a per item cost of $0.84. This is easily one of the cheapest tastiest meals I have had in awhile. Thanks, Trent!

Our frugal wedding

Moolanomy is having a contest for the best wedding tips and stories. I've been meaning to post about how we were paid just under $7000 for a wedding while living check to check, and how we had the best wedding ever on the dirty dirty cheap.

We were married 7 months ago. My wife and I are both from the South and we went back down to get married. The number 1 piece of advice is to consider hiring a wedding planner. Since we live together up north and all of our family lives below the Mason-Dixon lne a wedding planner was pretty much a necessity. Also, since I haven't lived in my hometown for over 7 years, I had no idea on where to have the reception.

We initially "hired" one of my ex girlfriends to be our wedding planner. She was someone who I had been friends with for many years before we dated for awhile in college. She remained a friend of mine after college. When I told her we were getting married, she offered her services as a free wedding planner since she wanted to get into event planning. I asked my fiancee, and she said no. We started looking into wedding planners in the area and it would cost us about $1500 bucks. My fiancee then though about it some more and agreed to using the ex girlfriend.

We started looking at different places to have our reception. We already knew the church we were going to get married in, so that wasn't really a consideration. The one problem with using a non professional as a planner was she had no connections, no discounts for using certain vendors. She also did not have the best ideas about where to hold the reception. We considered a bunch of areas, even the local zoo. When we didn't get much movement on the reception site, we decided to go with a professional planner. Remember, you get what you paid for, but that doesn't mean there aren't deals to be had.

We did a more extensive survey of planners in our area, and found one for $600. She was relatively new, but still had connections and discounts. The biggest deal we got by using the wedding planner was $500 off the photographer's package price, and an extra 3 hours of picture time. This saved us overall ~$1000 on the photographer services we got. Another way we cust costs on the photgrapher was to not get any developed pictures. In this era of all things digital, it really was a no brainer. We got over 1000 pics of getting ready shots, the ceremony, and the reception.

The wedding planner was also able to suggest a great place for the reception. It was in the covered courtyard area of one of the best restaurants in town. This cost us only $350 for four hours of reception time. This included 8 round tables that seated 8 people each, which was plenty for our small group. The wedding planner saved us about $500 by suggesting this place over other places we were considering that were much crappier. And since it was in the "courtyard area" it looked like a roustic european villa, already decorated with plenty of greenery which reduced the floral costs for the wedding dramatically.

This allowed us to only have to pay for centerpieces for the reception. We used the normal florist that our planner used, which got us ~25% off the normal prices. We also rented the vases for the centrepeices, which brought the price down $25 per centerpiece. We ended up only paying $650 for all the flowers for the reception, and boutineers for the groomsman, and parents. We did not need any flowers since we were married in a Catholic church that had seasonal flowers all year round.

We had a smallish wedding of only 75 people. This was mostly family with very close friends included. Having a small wedding will save you the most money because food will cost you the most.

We had a dinner reception and got the cheapest package for food, costing only $16.95 a person. Even the cheapest food at one of the best restaurants was extremely amazing. We were able to also substitute some of the more tastier pricier items into our menu by giving up things that we did not want. Always talk to the vendors and see if you can squeeze a little more out of them for the same price. Including the price of the of the site, and the catering that was done in house, we were able to get all of it, including some champagne for $1500. This was by far the costliest part of the wedding.

We "cheaped" out on the inventations and went to Micheals and got very nice cards for $30. We had them laser printed at staples which cost another $20. They looked great since they were laser printed, and saved us about $150 over ordering "real invitatations", none of which we really liked.

Clothing was one of the places where we splurged, and asked our bridal party to fork up some cash. My wife got her dream dress, and with all the alterations, it ended up costing $800 at David's Bridal. We had the bridesmaids buy their own dress, but they were able to choose a style they liked out of a subset my wife picked out, which made it more likely they would wear it again. It was also a nice red color, which also added to the possible mileage of the dress. The dresses were around $150, and since one of the bridesmaids had used the same color almost a year before, she was able to use one of her bridesmaid's dresses, which was free to her. Tux rental was $65 for the groomsmen and dads. Since we had 5 rentals, mine was free. My wife also used her sisters veil and crafted some mods to it to make it match her dress.

We also went with a DJ since we are not the dance all night type of people. We wanted to just have some nice background music after we did the special dances. The DJ cost us $500. The music was great and set a perfect ambience for the reception. Everyone was floating from table to table talking instead of having to shout over an annoying DJ with loud music.

Other incendtals for the wedding were 3 nights at a local hotel. This cost us $297 since we had called ahead and set up a wedding package. Just about every hotel will give your out of town guests a decent discount if you call ahead and set it up. We had 2 cakes that cost us $400 total. We bought table top disposable cameras that cost $100. We also drove into town, which cost us $250 for gas. We also tipped the priest $50, and the parents chipped in another $50. The chruch organist cost $150. My dad also chipped in for half of the rehersal dinner, so that only cost us $250.

The breakdown for the frugal wedding of the century is:

- Wedding Planner: $600

- Site rental and food for 75: $1500

- Photgraphy: $1000

- Chruch fee / officiant / ceremony music: $400

- Inventations: $50

- Clothes: $800

- DJ: $500

- Cake: $400

- Flowers: $650

- Rehersal dinner: $250 out of pocket.

- Travel: $550

- Wedding planner savings: $1750 minus her cost of $650, with a net of $1150 or 19%

Funniest Stimulus Check Mailer

Monday, May 5, 2008

My wife was going through the mail the other day, after she had read my post about our stimulus check, and told me that the stimulus check had come in the mail. I had already gone through the mail, so I knew what she was talking about. I told her that the envelope did not say "Tax Stimulus check enclosed" instead it said "Tax stimulus check idea enclosed." The funny part was:

It was from a collections company.

Calling all PF bloggers and readers!

My money and my life has fallen off the financially responsible bandwagon. She needs some encouragement STAT. Head on over and comment some pick me ups to let her know she can get back on track!

Nowhere to be found

One of the reasons why I would like to be debt free, other than the obvious one of not having to owe anyone money, is to be off the grid. That is one of my retirement goals, and when I know I'll have enough money saved up.

I don't want a mortgage, I don't want a utility bill, I would rather not pay taxes, and I might not even have a mailbox. Just give me my 2 acres in the foothills of the Smokies, my house, my family, a 6 foot brick wall surrounding my property, and I'll consider putting in a drawbridge so you can cross the shark filled moat.

Realistically though, when I retire, I do want to be off the grid as much as possible. I want solar panels that generate income. I want to move to Tennessee where they don't have a state income tax, only a 9% sales tax, and a state government that is now fiscally responsible enough to have multiple sales tax free weekends throughout the year because they have surpluses.

Comment on what kind of lifestyle you are saving towards for your retirement.

Man of the earth

Sunday, May 4, 2008

Well, I started my garden today. I made a couple of self watering seed starters today, and stopped off at the local garden store and bought some beefsteak tomatoes seeds, some california sweet pepper seeds, and some lettuce seeds. I got the instructions on the seed starters from this site. They used cotton rope for wicks, but I was able to recycle even more.

Have you ever had a pair of jeans that are so comfortable, and even when they start to rip you still wear them? Well I had a pair that had a vertical rip in the middle of the left leg from the waist to the knee. I would tell my wife it was for easy access, but for some odd reason she would always just roll her eyes at me. I don't know why. Today those jeans were finally retired, and got ripped up and turned into wicks. I tried using twine, but after 6 hours the twine had not soaked any water into the upper portion, so I had to take those out. The jeans worked out much better.

Currently the seed starters do not have any greenhouse style covers, but they will once we finish off another couple of 2 liters of Mountain Dew. I'll post some pics once the seeds start sprouting.

I also mowed the grass today with my new to me riding mower. It ws very fun. it sitll took awhile to cut, but I actually cut it, and had some energy after cutting it, even after going into work for 6 hours. Yea!

Grocery Savings

Saturday, May 3, 2008

So I have returned from Sams Club victorious! The grand total was $144.29. While this does shoot what I normally spend on a trip to the regular store in the foot (normally about $80-$90) I actually saved quite a bit off of regular prices. Most people will read this and say "Duh", but the amount I actually saved was quite suprising. Here's the break down:

- Basics: $74.49

- Home items: $36.28

- Indulgence: $5.84

- Side Dishes: $7.60

- Quick Meals: $9.71

- Cleaning Products: $0.00

- Coupons: $0.00

There were 2 cool things about this trip. Sams had 8 cfl bulbs for $10.86. This is only marginally more expensive than traditional bulbs at the regular stores I go to. CFL bulbs cost $3-$4 a bulb when I normally look. That was pretty cool. The second cool thing was how much I saved. I plugged the normal prices into the spreadsheet for the items I bought and the total was astounding: $249.44 That price blew me away. I would never consider paying that much at teh grocery store. I would most likely make 2 trips. I guess that is the biggest problem I had with Sams before this.

Whenever I would leave Sams, I would feel like I barely bought anything, but always have a bill over $100. I always knew I bought more than I thought I did, but it was usually demoralizing. Now after seeing that I saved over $100 buy shopping there, you better believe that I'll be heading there every 2 weeks now.

daily goings on

Well, in my effort to reduce the amount of money we spend on groceries, I am going to head out to Sams today. Normally I'll shop at Meijers or Walmart, but I am wanting to make some bread items, and I need more flour. I'll update you when I get back with the grocery breakdown. Maybe they'll have some garden starter stuff so I can start growing our own veggies.

Other than that and work, it looks to be a pretty ho hum weekend here. It's raining today, but I'll be able to use the lawnmower tomorrow, after I get home from work. Boooo.

Hey, Dirty. Baby I got your money

Friday, May 2, 2008

Well actually, as it turns out the IRS will still have my money for another couple of weeks. I checked the ol' checking account today, and no stimulus payment. According to the original schedule I should have had my money by now, not even considering the acceleration period. So I went searching for info.

The IRS has a "where's my money" link. So I went there, and they had no information. It actually said "we have no information to give you." What?!? How can a schedule program not work when I give you all of the correct information. Nonetheless, I was not to be thwarted. I also saw a contact us link So i looked up the 1800 number and dialed away. I mean, it did say "Live assistance available from 7AM to 10PM local time."

I got stuck in an automated system. I figured I'd still give it a try and see if this schedule program could tell me where my money was. To no avail, though. It also said that it had no information to share. Bummer. I redialed the number thinking that there would be some option to talk to someone. There wasn't.

I got transferred to their stimulus "hotline". No option to talk to someone. Oh yeah, and if you hit zero too many times, they'll hang up on you. But finally I reached the end of my rope. I just didn't type any numbers, thinking that I would confuse the system and it would let me talk to someone since the system would think that I didn't know how to operate a touch tone phone, even though I called on one. Instead it went to an voice automated system. Aaarrrggggghhhh! As I was about to give up, I shouted, "I just want to talk to someone!"

And miraculously it was so. I had been transferred to a real live person.

I asked the gentleman where my money was, and told him that he would have to start paying me points on the vig if he were to keep my money any longer. He asked me what the last two of my social was, and I told him 00. He asked if I direct deposited my refund. I told him I had. He then wondered why I had not gotten my money, and promised to pay points on the vig if I did not get it rapido. Well not really. Instead he asked me for my entire social, I gave it to him, and also told him I filed through HR blocks online website for Direct Deposit.

He asked me if I paid for the HR Block services with my refund, and I said yes.

He then went on to inform me that this would cause me to receive a paper check. "Wait, I filed electronically. Hell, I even filled out the form electronically. I paid for the services electronically. I even had the refund applied electronically. Not once did I pick up a pen and paper anywhere in this transaction."

I saved 200 trees by my estimation.

"And you are telling me that I get a paper stimulus check?" "Yes." He replied. I thanked him and told him he had done a very good job, which he had. I now no longer have to wonder why a coworker got their stimulus check on a Sunday?!?!?!?!?!?!?! and can now wait another 3-4 weeks for my stimulus check to come in the mail, go down to my local bank branch which I have done I think only twice this year anyway, and talk to a local teller and have her deposit my money.

Thanks IRS for wasting my time by not running the last leg of the race with a bionic, electronic leg.

Although, I am able to help people out. If you too want to talk to a real live IRS person, call 1-800-840-1040 (haha) and hit 1 to speak in english or ocho to speak in spanish, 7 to get transferred to the stimulus help line, do not hit any buttons so that it switches to the voice prompt instead of the touch tone, and whine, "All i want to do is talk to someone." This worked for me.

basicsavings

Thursday, May 1, 2008

w00t! The second automatic deposit into our ING savings account today. We now have a whole $250 in our savings. This is by far the most we have ever had in our savings outside of bonus time. Go us!